FinStack — A FinTech Startup & Technology Landscape 🪙

Financial technology, or “Fintech”, is a fast growing arena with new technologies, companies and innovations. The landscape is constantly evolving with entrepreneurs often lured by the vast sums of capital at play in financial markets.

Fintech was one of the most prolific sectors for venture capital before the current downturn came to pass. The Economist¹ highlighted last year how:

“The venture-capital boom is a risk for investors — and a gift for everyone else”.

A nod to all the freebies, below cost services and offers consumers will receive from these new VC-backed entrants. In practice they are using their war chests to try and lure customers into their products and services for the promise of earning their customer lifetime value, or “CLTV” for short.

However, finance is an area with inherently high switching costs — Who on earth wants to regularly move their banking provider and transfer standing orders, direct debits and automated payments?

With the addition of, frankly, quite insane cost of customer acquisition (CAC) — for example, the cost per click (CPC) for the term “credit card” is floating around $10.87 according to Semrush², a search engine marketing platform — this is certainly no playground!

Incumbents such as VISA (NYSE:V) and Bloomberg maintain healthy dynasties with fat profit margins despite being almost four decades old. This is a true sign of an enduring business model.

More recent insurgents such as Revolut and Stripe have found their own niches. They exploded past conceptions of what is possible in mobile-first banking and payments infrastructure, respectively. Noticeably, despite gargantuan valuations, and private fundraising, few of these companies are publicly listed on global stock exchanges.

Somewhat predictably the incumbents are fighting back with behemoths like JP Morgan launching Chase in the United Kingdom as a mobile first offering to compete with neo-banks like Monzo, Revolut and Starling Bank.

In some ways the whole sector is reminiscent of the battles played out in the early days of the Internet but potentially with even more at stake. You only have to look East to China to see the awe inspiring success of financial one-stop-shops like Ant Group³ (formerly known as Ant Financial). In August this year Bloomberg estimated its market value at $75 billion. Officially launched in 2014, but the fascinating history stretches back to 2004 with the creation of AliPay. A reminder that good things come to those who wait!

FinStack — Version 1.0 🗺

As with all maps the purpose of this exercise is to give a sense of perspective and allow one to navigate the Fintech landscape.

Broadly the map is split in Consumer (i.e., B2C) and Business (i.e., B2B) business models from left to right and vertically into five distinct “layers”:

- Intelligence Layer 🧠 — this is a relatively new layer made possible by recent advancements in data processing capability, data availability and advanced machine learning techniques from deep neural networks to natural language understanding (NLU). This includes Ntropy (intelligent transaction enrichment), CausaLens (causal AI decision making platform) and 9fin (leveraged finance intelligence platform).

- Services Layer 📱 / 🏦 — the layer which we experience and interact with on a daily basis as consumers or business owners and employees. This layer is split into B2B and B2C business models. The services layer includes banking by neo-banks like Monzo, Revolut and Tide and N26. Several personal finance “super apps” or assistants such as Emma and Cleo. Other scale-ups which have experienced strong growth in recent years include Brex, Ramp and Robinhood.

- Infrastructure Layer 🛣 — A technically challenging, however, incredibly important layer is the core banking and financial services infrastructure layer on which B2C and B2B services are built atop. This includes companies such as Thought Machine, R3 and ConsenSys. This layer has seen vast investment sums from venture capital and private equity in the last half decade.

- Payment Layer 💳 — this is a layer in which vast fortune have been made as the companies who own transaction are in an enviable position of being able to tax and rent seek on top of the payment rails they have invest in and deployed. They grease the wheels of the capitalist economy and reap the benefits with sustainable profit margins. This include stalwarts Mastercard and VISA but also Stripe, PayPal and it’s subsidiaries such as Braintree.

- Data Layer 🧮 — the 1s and 0s or more often than not JSON, CSV and SQL queries that power the financial services industry — many long standing behemoths such as Oracle and Microsoft have strong offerings alongside open source options from more recent entrants like MariaDB (made by the original developers of MySQL and guaranteed to stay open source, MySQL is owned by Oracle after they were acquired by Sun Microsystems) and Hopsworks (hosted Feature Store with a focus on data governance) by Logical Clocks.

Fintech — The Land of Unicorns 🦄

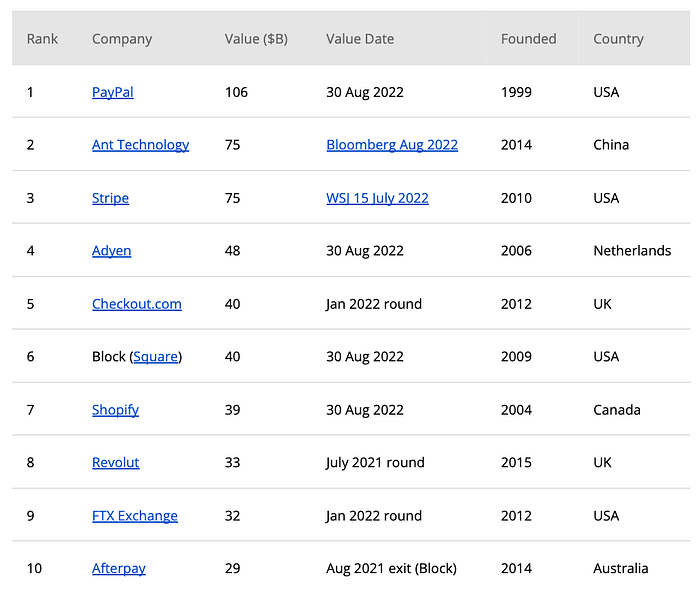

Finance is such a gargantuan sector. In the UK alone the sector is estimated by Her Majesty’s government to be worth some £173.6 billion per annum, or 8.3% of total economic output according to the House of Commons Library⁴. That is exactly why it is such a promised land of “unicorns” (i.e., companies valued over $1B) and even the odd “centurion” (Paypal is now valued >$100B). That may be why so many founders aspire to build, but so few actually manifest, the “next big thing” in fintech.

According to Fintech Labs⁵ there are currently 321 Fintech unicorns globally, below are the Top 10 by market value:

What is fascinating is that Fintech is a truly global industry. USA (PayPal, Stripe, Block, FTX Exchange) accounts for 40% of the Top 10 but five other countries are represented, UK (Checkout.com), China (Ant Technology), Canada (Shopify), Australia (Afterpay) and the Netherlands (Adyen).

This is a global battlefield and it’s not for the faint of heart!

Venture Capital Investment Trends in Fintech 💸

I have invested personally, either via my own angel investing or investment firms, in which I have been a founding partner, AI Seed and Kintsugi (Ad)ventures in 70+ startups in the last decade.

Not all are Fintech. Sector wise, I invest broadly in a thesis of “advanced technologies for people and planet”, therefore several are in Healthcare, Agritech, Biotech, Quantum Computing or plain, good old fashioned Enterprise SaaS.

Unsurprisingly, it is often the boring companies that don’t sound exciting but grind out sales and build products every day for a minimum 7–8 years that end up building long standing enterprises in the market they dare to enter. However, Fintech is a very competitive landscape due to the large stakes at play.

Startups, especially those that bring new, advanced technologies to market are emphatically not an easy path to follow. Trust me, I’ve been there, done that, got the t-shirt. Even saw Marc Benioff on stage at Dreamforce with Lenny Kravitz back in the mid-2010s after we sold a company to Salesforce.com.

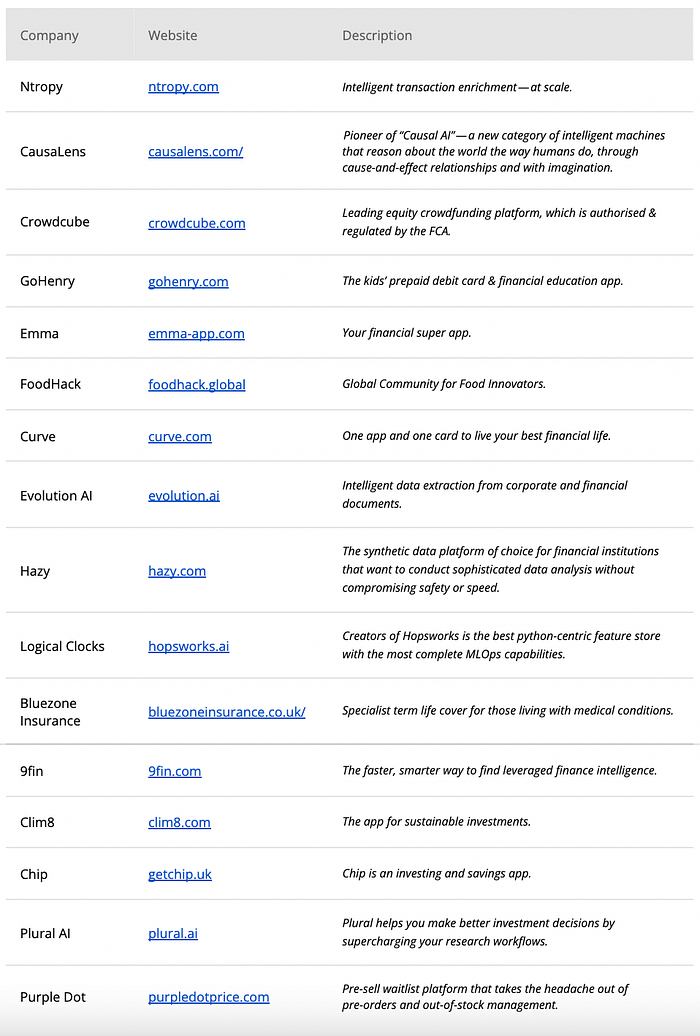

Some examples of startups I’ve supported early on in their journeys which are now making waves in the Financial Services sectors include:

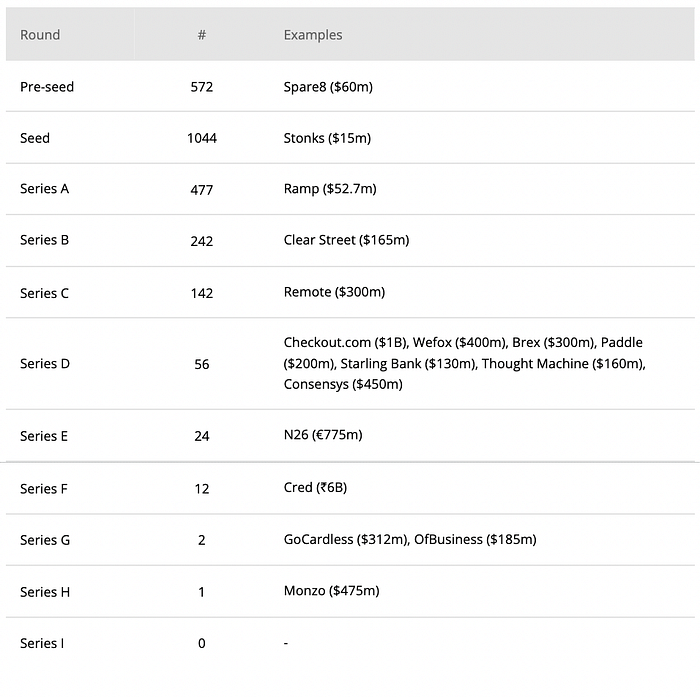

It is far too early to pick outright winners but there are some great founders and therefore great companies in that portfolio. Looking at the broader market we see a continuation of strong investment into Fintech with 2,000+ private funding rounds into the category in the past twelve months according to CrunchBase data.

The table below shows private Fintech funding rounds in the last 12 months (Crunchbase 2022) the number of rounds by stage with some examples of well known companies funding rounds:

Conclusions 🧐

An old friend and venture capitalist Nathan Benaich at Air Street Capital seems to have a general dislike of any kind of mapping whether it is the Bloomberg Beta map of Machine Intelligence or another CB Insights map of something or other!

This is categorically not the first attempt to map “Fintech” and there is some decent prior work such as Make Cents: A Fintech Market Map⁶ by Medha Agarwal at Redpoint Ventures. This “FinStack” map intends to draw meaningful visualisation of the various technologies in the same way a develop or engineer would create a system diagram to explain a technology stack to new hires.

Hopefully by the end of reading this we have increased the general education level about Fintech and the technologies being built today by leading edge startups like Ntropy, CausaLens and many, many others.

Why?

Well for two reasons, one is selfishly to look back on these investments and uncover any learnings or insights. Clearly sixteen deals in ten years is not going to give any statistical significance in terms of longitudinal studies of venture capital investment in Fintech.

However, it’s enough to do some “pattern matching”, as VCs like to say. Otherwise known as, explicitly stating one’s own confirmation biases with overconfidence in one’s own ability to predict the future from the past!

A personal thank you to several individuals who spent time reading drafts and giving thoughtful feedback, pointers and questions including Naré Vardanyan, Ilia Zintchenko, Tom Groenfeldt, Yoram Wijngaarde, Steven Hunter, Alejandro Ortega and Darko Matovski.

Finally, feel free to leave any feedback, comments or omissions in the comment section below and I will endeavour to iterate and revised the landscape in due course!

References

¹ Technology unicorns are growing at a record clip | The Economist (2021)

² Semrush — Keyword Overview: “credit card“(2022)

³ Ant Group Official Website — The History (2022)

⁴ Financial services: contribution to the UK economy — House of Commons Library (2022)

⁵ The 321 Fintech Unicorns of the 21st Century (Sep 2022)

⁶ Make Cents: A Fintech Market Map — by Medha Agarwal (2022)